Table of Contents

Corporate tax risk management is what separates companies that operate with confidence from those scrambling when tax auditors arrive. corporate tax risk management. Every organization that files a tax return carries exposure, whether you’re running a multinational corporation or managing a mid-sized enterprise.

The difference in outcomes rarely comes down to luck or aggressive tax planning. It comes down to structure. Having a systematic approach that spots risks early, implements smart controls, and creates visibility for better decision-making.

What Is Tax Risk?

Tax risk refers to the possibility that a company may face financial penalties, regulatory scrutiny, reputational damage, or operational disruption due to non-compliance, misinterpretation of tax laws, weak internal controls, or inadequate documentation.

In 2026, tax risk is no longer limited to filing errors. It extends to governance gaps, regulatory change management, cross-border reporting obligations, and the strength of internal compliance systems.

This guide breaks down what corporate tax risk management actually involves, why it matters beyond just ticking compliance boxes in 2026, and how your organization can build frameworks that reduce exposure while supporting confident financial leadership.

What Is Corporate Tax Risk Management?

Corporate tax risk management is how your organization systematically identifies, assesses, and mitigates risks tied to tax obligations and positions.

Think about corporate tax risk like this: it’s the possibility that your tax position, whether through filing mistakes, interpretation gaps, documentation failures, or structural choices, creates financial penalties, regulatory scrutiny, reputational damage, or unexpected liabilities.

Every organization carries tax risk because tax systems stay complex, change constantly, and require interpretation. Even when you’re trying to accomplish everything correctly, differences in how you apply tax laws, document transactions, or report positions can create compliance risk that surfaces years after you’ve submitted filings.

Why Every Organization Has Tax Risk?

Your operations might seem straightforward, but corporate tax involves judgment calls at multiple levels.

Transfer pricing decisions. How you classify expenses. When you recognize revenue. Whether certain costs qualify as deductible.

Each choice carries inherent uncertainty because legislators write tax codes broadly, yet practitioners must apply them to specific situations.

In my experience, regulatory authorities don’t always see things the way organizations do. What seems defensible internally might not survive regulatory review. Guidance that worked last year might conflict with updated interpretations this year.

That gap between what you intended and what regulators expect?

That’s where tax risk lives.

Beyond interpretation issues, tax risk stems from operational realities. Deadlines slip by. Teams fail to retain documentation properly. Systems don’t communicate with each other effectively. Finance departments work under resource constraints.

These aren’t excuses. They’re realities that create exposure when you’re not actively managing them properly.

How Tax Risk Differs from Tax Avoidance

Let’s clear up a common confusion: tax risk management has nothing to do with enabling aggressive tax avoidance or helping organizations push legal boundaries.

Tax avoidance involves strategies, sometimes legally questionable, that minimize tax liability through arrangements that might technically comply with legal wording but violate legislative intent. These typically involve complex structures designed primarily for tax benefit rather than commercial substance.

Tax risk? That exists even when you’re trying to do everything correctly.

It’s the risk that:

- You classify a legitimate business transaction incorrectly

- Documentation supporting a deduction turns out incomplete

- Your team misses a filing deadline because of process failure

- Your interpretation of a new regulation proves wrong

- A routine audit uncovers an unintentional error from three years back

Managing tax risk isn’t about being clever with tax codes. It’s about maintaining discipline with compliance, documentation, governance, and controls so routine tax obligations don’t become sources of unexpected financial exposure or regulatory problems.

Why Organizations Can’t Treat Tax Risk Management as Optional

Some companies treat tax risk management as something only the largest corporations need.

That’s a complete miscalculation.

Every organization subject to corporate tax faces compliance obligations, regulatory oversight, and financial reporting requirements. The complexity might differ, but consequences of mismanagement don’t discriminate by company size.

Leave tax risk unmanaged, and companies will face:

- Financial exposure through penalties, interest, and retroactive adjustments

- Regulatory scrutiny that triggers deeper audits and ongoing monitoring

- Reputational damage when tax issues become public or affect stakeholder confidence

- Operational disruption when leadership diverts attention to resolving avoidable problems

Companies treating tax risk as “someone else’s problem” or assuming their external accountants handle everything typically discover gaps only when it’s too late to fix them without consequences.

Effective corporate tax risk management doesn’t require massive resources or complex systems. It requires intentionality. You must treat tax obligations as part of overall corporate governance rather than a back-office function running on autopilot until something breaks.

Organizations managing corporate tax risk well aren’t necessarily those with the biggest budgets or most sophisticated technology. They’re the ones recognizing tax risk as a governance issue, building structured processes around it, and maintaining discipline in execution.

Why Corporate Tax Risk Matters to Organizations

Tax risk isn’t some abstract concept mattering only during audits. It creates real, tangible consequences affecting financial performance, strategic decision-making, and organizational reputation.

Understanding why corporate tax risk matters helps leaders prioritize it appropriately, not as a compliance checkbox, but as a core component of sound corporate governance.

Financial Consequences of Unmanaged Tax Risk

Unmanaged tax risk hits you financially first and hardest.

When tax positions don’t survive review, you face penalties, interest charges, and retroactive adjustments directly impacting your bottom line.

Regulators impose penalties for late filings, underpayments, or inaccurate reporting that can be substantial. Interest accrues from the original due date, compounding over time when you don’t identify and correct issues quickly. In cases involving material misstatements or repeated compliance failures, regulatory authorities impose additional fines beyond simple corrections.

Beyond direct penalties, financial exposure includes the cost of resolving issues once you identify them. Legal fees pile up. Advisory fees add to the burden. Internal resources divert from regular responsibilities to address audit queries, reconstruct documentation, or defend positions that should have been properly supported from the start.

Consider the opportunity cost too.

Cash tied up in disputed amounts or held in reserve for potential liabilities isn’t available for operations, investments, or strategic initiatives. Uncertainty about tax exposure complicates financial planning and can affect credit ratings, borrowing capacity, and investor confidence.

Organizations sometimes underestimate these financial consequences because they think of tax as something accountants’ handle. But when tax risk materializes into actual liability, it stops being an accounting problem.

It becomes a business problem affecting cash flow, profitability, and financial stability.

Reputational and Governance Implications

Tax issues becoming public, whether through regulatory enforcement actions, financial restatements, or media coverage, carry reputational risk extending beyond immediate financial impact.

Stakeholders pay attention to how you manage obligations. Investors, board members, customers, and employees all form judgments based on whether your company appears to operate with integrity and competence in meeting regulatory responsibilities.

When tax problems surface, the narrative often centers on governance questions.

Was leadership paying attention? Did appropriate controls exist? Did the organization take compliance obligations seriously?

Even when tax issues result from honest mistakes rather than intentional wrongdoing, reputational impact can be significant. Stakeholders wonder: if you can’t manage tax obligations properly, what else might be falling through the cracks?

For publicly traded companies, tax controversies affect stock prices and analyst sentiment. Private companies find they complicate fundraising, acquisition discussions, or partnership negotiations. Organizations in regulated industries discover that tax compliance failures trigger broader regulatory scrutiny extending into other operational areas.

You build reputation slowly and damage it quickly.

Organizations experiencing publicized tax problems often spend years rebuilding stakeholder confidence, even after resolving underlying issues.

Regulatory Scrutiny and Enforcement Trends

Regulatory authorities worldwide have become more sophisticated and aggressive in their approach to corporate tax compliance. Technology improvements allow tax agencies to analyze data more effectively, identify patterns suggesting risk, and target audits more strategically.

Companies showing signs of weak tax risk management, such as inconsistent filings, incomplete documentation, unexplained positions, or late submissions, often find themselves subject to deeper scrutiny. Once you’re on a regulator’s radar for any reason, you face higher likelihood of ongoing monitoring and repeated audits.

Enforcement trends have shifted toward holding individuals accountable, not just organizations. Senior executives and board members increasingly face personal liability questions when tax governance failures occur. This reality changes how leadership teams think about oversight responsibilities related to tax risk assessment.

International cooperation among tax authorities has intensified too. Information sharing agreements mean issues in one jurisdiction trigger questions in others. Organizations operating across borders can’t treat each country’s tax obligations in isolation; they need coordinated approaches recognizing how regulatory authorities work together.

The trend stays clear: tax authorities have more tools, more data, and more willingness to challenge corporate positions than ever before. Organizations that haven’t invested in structured tax risk management operate in an environment becoming progressively less forgiving of gaps and oversights.

Impact on Financial Reporting and Decision-Making

Tax risk affects more than compliance; it influences financial reporting accuracy and strategic business decisions.

From a financial reporting perspective, uncertain tax positions require disclosure. Your team needs to estimate potential liabilities, maintain appropriate reserves, and explain material tax risks in financial statements. When you haven’t properly identified and assessed tax risk, financial reporting becomes less reliable, auditors may qualify opinions, and stakeholder confidence erodes.

Tax considerations also factor into major business decisions.

Mergers and acquisitions involve extensive tax due diligence. Restructuring decisions carry tax implications. Investment choices depend partly on after-tax returns. When you don’t properly understand tax risk, leadership makes these decisions with incomplete information.

Leaders can’t make fully informed strategic choices without clarity about their organization’s tax position and potential exposures. Uncertainty about tax risk creates uncertainty about financial performance, which ripples through planning, forecasting, and resource allocation decisions.

Organizations managing tax risk effectively make decisions with confidence. They know their positions are defensible, their documentation is solid, and teams have understood and appropriately reserved their exposure. Such clarity supports better decision-making across the organization, not just within the tax function.

Common Sources and Example of Corporate Tax Risk

Understanding where corporate tax risk typically originates helps you focus tax risk management efforts on areas most likely to create problems.

While every organization’s risk profile stays unique, certain sources of tax risk appear consistently across industries and jurisdictions. Recognizing these common risk sources represents the first step toward managing them effectively.

Interpretation of Tax Laws and Regulations

Legislators write tax codes broadly, requiring interpretation when practitioners apply them to specific situations. Different professionals can reasonably reach different conclusions about how a particular rule applies to a particular transaction.

This interpretive uncertainty creates tax risk because organizations must take positions on returns reflecting their interpretation, knowing regulatory authorities might interpret the same rules differently.

Common Interpretation Challenges

Classification Questions

Classification questions determine whether something receives treatment as capital or ordinary, deductible or non-deductible, current or deferred. These classifications have material tax consequences but often involve judgment rather than bright-line rules.

Timing and Recognition Issues

Timing issues around when you recognize income or when expenses become deductible. Accrual accounting, revenue recognition standards, and matching principles create complexity requiring interpretation when teams apply them to real transactions.

Transaction Characterization

Characterization of transactions where tax treatment depends on substance over form, economic substance doctrines, or step transaction principles. What seems clear from a commercial perspective may receive different analysis from a tax perspective.

New Regulation Application

Application of new regulations where guidance stays limited, evolving, or ambiguous. When tax laws change, there’s often a period of uncertainty while regulatory authorities issue clarifying guidance and audits test positions.

Interpretation risk doesn’t mean you shouldn’t take defensible positions. It means you need to document your reasoning, understand alternative interpretations, assess the likelihood your position will face challenge, and make informed decisions about which positions are worth defending.

Documentation and Record-Keeping Gaps

Even when tax positions are technically correct, inadequate documentation can make them indefensible during audits.

Regulatory authorities expect you to support tax positions with contemporaneous documentation: records created when transactions occurred, not reconstructed years later when questions arise.

Types of Documentation Gaps

Missing Supporting Records

Missing supporting records for deductions, credits, or other beneficial positions claimed on returns. Without documentation, positions that are entirely legitimate become impossible to defend.

Incomplete Transaction Records

Incomplete transaction records that don’t capture sufficient detail to demonstrate business purpose, commercial substance, or arm’s-length nature of arrangements that might face questioning.

Inadequate Position Explanations

Inadequate explanations for positions involving judgment or interpretation. When returns reflect non-obvious positions, internal memos or analyses explaining the reasoning help demonstrate positions were taken thoughtfully rather than carelessly.

Poor Retention Practices

Poor retention practices resulting in documents being discarded before statute of limitations periods expire. Many organizations don’t realize how long they need to retain tax-related records or don’t have systems preserving records for appropriate periods.

Disorganized Filing Systems

Disorganized files making it difficult to locate relevant documentation when needed. Having documentation isn’t useful when you can’t find it efficiently when audit questions arise.

Documentation risk is particularly insidious because it doesn’t manifest until years after transactions occur. By the time you discover documentation gaps during audits, it’s too late to create what should have existed from the beginning.

Transactional and Structural Risks

Complex transactions and organizational structures create tax risk through the positions and elections they require.

Key Transaction Types That Create Risk

Related Party Transactions

Related party transactions between affiliated entities require transfer pricing documentation, intercompany agreements, and defensible pricing methodologies. These arrangements face heightened scrutiny because regulatory authorities want to ensure pricing reflects arm’s-length terms rather than tax-motivated allocations.

Cross-Border Transactions

Cross-border transactions involve multiple tax systems, treaty interpretations, withholding obligations, and permanent establishment considerations. The interaction between different countries’ tax rules creates complexity requiring specialized knowledge to navigate correctly.

Reorganizations and Restructurings

Reorganizations and restructurings trigger tax consequences depending on meeting specific requirements for tax-free treatment. Missing a technical requirement can convert what you intended as a tax-free reorganization into a taxable event with immediate consequences.

Financing Arrangements

Financing arrangements raise questions about debt versus equity classification, thin capitalization, interest deductibility, and economic substance. How you document and operate financing structures matters as much as how you design them.

IP and Intangible Asset Transactions

IP and intangible asset transactions involve valuation challenges, cost-sharing arrangements, and questions about where economic value really gets created versus where legal ownership sits.

These transactional and structural risks often require specialized expertise to identify and manage. Your team can’t rely solely on general tax knowledge; they need access to professionals understanding the specific rules and regulatory concerns applying to complex arrangements.

Operational and Process Failures

Even when organizations have the right technical expertise and intentions, operational realities create tax risk through process breakdowns and system limitations.

Common Operational Breakdown Points

Communication Gaps

Inadequate communication between tax teams and business units means tax implications aren’t considered when transactions receive structuring. By the time tax becomes involved, commercial deals are already finalized in ways creating unnecessary tax complexity or exposure.

System and Technology Limitations

System limitations don’t capture information needed for tax reporting or generate data in formats not aligning with filing requirements. When tax teams spend excessive time manually manipulating data, errors become inevitable.

Resource Constraints

Resource constraints result in rushed filings, limited review, or deferred maintenance of tax processes. Tax departments are often under-resourced relative to the complexity they’re managing, creating execution risk even when knowledge and intentions stay sound.

Knowledge Transfer Failures

Turnover and knowledge gaps occur when key tax personnel leave and institutional knowledge isn’t properly documented or transferred. Tax positions often depend on understanding history and context not obvious from reviewing current year returns.

Cross-Functional Coordination Breakdowns

Lack of cross-functional coordination happens when tax implications aren’t considered during financial reporting, treasury, legal, or operational decision-making processes.

Teams can prevent operational and process failures through better systems, clearer accountabilities, and more disciplined workflows. But they persist in many organizations because they’re not obviously tax problems; they look like general operational challenges that happen to have tax consequences.

Effective tax risk management also depends heavily on documentation discipline. Many organizations align their internal processes with established regulatory expectations, such as IRS documentation requirements, which emphasize contemporaneous records, defensible positions, and clear audit trails to support reported tax outcomes.

Identifying Corporate Tax Risks Before They Escalate

Organizations managing tax risk most effectively don’t wait for problems to surface. They build processes identifying potential issues early, when they’re still manageable and before they trigger regulatory scrutiny or financial consequences.

Proactive tax risk identification requires intentional effort, but it’s far less costly and disruptive than dealing with materialized risks that teams could have prevented.

Tax Risk Assessments and Reviews

Regular tax risk assessments provide structured opportunities to evaluate where exposure exists and whether current controls are adequate.

Effective assessments go beyond reviewing compliance status. They examine the full range of tax positions, consider changes in operations or regulations creating new risks, and evaluate whether documentation and governance practices meet current standards.

A comprehensive tax risk assessment typically covers:

Review of tax positions taken on recent returns to verify they’re still defensible, properly documented, and consistent with current interpretations of applicable rules.

Analysis of new or unusual transactions occurring during the period to ensure tax implications were properly considered and that positions taken reflect sound reasoning.

Evaluation of changes in business operations that might create new tax obligations, filing requirements, or compliance risks not previously relevant.

Assessment of regulatory environment changes including new laws, regulations, guidance, or enforcement priorities affecting how you should evaluate existing positions.

Testing of controls and processes to confirm they operate as designed and catch errors or issues before they make it into filed returns.

Conduct tax risk assessments regularly: at minimum annually, and more frequently for organizations with high complexity or rapid change. Document them thoroughly so there’s a record of what received review, what issues were identified, and what actions were taken in response.

The goal isn’t achieving zero risk: that’s neither possible nor necessary. The goal is understanding where risk exists, making informed decisions about which risks are acceptable and which need mitigation measures, and ensuring significant exposures aren’t sitting unidentified until external parties discover them.

Internal Controls and Reporting Systems

Strong internal controls create the foundation for identifying and preventing tax risk before it materializes.

Tax-specific controls should address:

Data accuracy and completeness through reconciliations verifying information flowing into tax calculations and returns matches source systems and is complete for the reporting period.

Review and approval processes ensuring multiple qualified individuals examine tax positions before your team files returns, creating opportunities to catch errors or questionable positions.

Deadline tracking and compliance calendars preventing missed filings through systematic monitoring of obligations across all relevant jurisdictions.

Documentation requirements specifying what support needs gathering and retaining for different types of positions, making proper documentation a routine part of transaction processing rather than something reconstructed later.

Segregation of duties preventing any single individual from controlling all aspects of tax compliance without independent oversight or verification.

Reporting systems should provide leadership with visibility into tax risk,

through regular updates highlighting:

- Significant positions taken or contemplated

- Changes in risk profile based on operational or regulatory developments

- Compliance status across all filing obligations

- Results of internal reviews or external audits

- Open issues requiring resolution or management decision

When internal controls are properly designed and operate effectively, many tax risks receive identification and correction before you file returns. Problems slipping through receive quick detection rather than compounding over multiple periods.

Role of Internal Teams vs External Advisors

Most organizations rely on some combination of internal tax expertise and external advisors. Understanding how these resources should work together helps maximize tax risk identification capabilities.

Internal teams bring institutional knowledge, operational context, and day-to-day involvement that external advisors can’t replicate. They understand how the business works, have relationships across functions, and can spot issues as they develop rather than discovering them during year-end reviews.

Internal tax functions should focus on:

- Routine compliance and reporting

- Day-to-day questions arising from operational activities

- Coordination with finance, legal, treasury, and business units

- Monitoring regulatory developments relevant to the organization

- Oversight of external advisor work to ensure it’s appropriate for your specific circumstances

External advisors provide specialized expertise, regulatory insights, technical depth in specific areas, and independent perspectives complementing internal capabilities.

External advisors are typically most valuable for:

- Complex technical issues requiring specialized knowledge

- Significant transactions falling outside routine operations

- Independent reviews of positions where external validation adds credibility

- Regulatory disputes or audit defense where specialized experience matters

- Keeping current on regulatory changes across multiple jurisdictions

The most effective approach combines internal and external resources strategically. Internal teams handle routine matters and coordinate overall tax risk management, while external advisors provide specialized input on complex issues and periodic independent reviews validating the overall approach.

Problems arise when you rely too heavily on one or the other. Over-reliance on external advisors without strong internal oversight creates risks because external advisors may not fully understand operational realities or organizational priorities. Over-reliance on internal resources without access to specialized expertise creates risks when complex issues arise exceeding internal capabilities.

Early Warning Signs Organizations Overlook

Certain indicators suggest tax risk may be building even when obvious problems haven’t surfaced yet. Organizations paying attention to these warning signs can address issues before they escalate.

Seven Critical Warning Signs

1. Recurring Audit Adjustments

Recurring audit adjustments on similar issues across multiple years suggest systematic problems in how you’re evaluating or documenting positions. When the same types of items keep receiving adjustments, it signals internal processes aren’t adequately addressing the underlying issue.

2. Difficulty Responding to Inquiries

Difficulty answering regulatory inquiries or producing requested documentation indicates gaps in record-keeping or understanding of positions taken. If your team struggles to explain or support positions during routine inquiries, those positions probably won’t hold up under more intensive scrutiny.

3. Complexity Outpacing Controls

Increasing complexity without corresponding control enhancements means risk is growing faster than your ability to manage it. As operations expand into new jurisdictions, new transaction types, or new structures, controls need evolving proportionally.

4. Knowledge Loss from Turnover

High turnover in tax or finance functions creates knowledge gaps and continuity risks. When institutional knowledge walks out the door without proper documentation or transition, important details and context can be lost.

5. Frequent Restatements

Frequent restatements or corrections to filed returns indicate quality control issues in the preparation process. While occasional corrections are normal, patterns suggest systematic problems with review processes or data accuracy.

6. Leadership Disconnect

Leadership disconnect where executives responsible for tax governance can’t articulate the organization’s key tax risks or current positions suggests inadequate reporting and oversight.

7. Chronic Resource Constraints

Resource constraints resulting in chronic backlogs, deferred projects, or inability to address known issues create accumulating risk eventually manifesting in bigger problems.

Why Early Detection Matters

These warning signs rarely trigger immediate consequences, which is exactly why teams overlook them. By the time obvious problems surface, underlying issues have often been building for years. Organizations treating early warning signs seriously can address root causes before they create material exposure.

Internal Warnings Mirror External Audit Triggers

Here’s what makes these warning signs particularly important: tax authorities are watching for the same issues. Inconsistent financial reporting, persistent losses, poorly documented intercompany transactions, these aren’t just internal process problems. They’re well-known audit triggers that regulatory authorities routinely target, particularly in transfer pricing examinations.

The pattern is clear: many external risks that trigger audits actually originate from internal gaps you left unaddressed.

However, internal warning signs aren’t just red flags for your team; they’re exactly what tax authorities look for during reviews. Inconsistent financial reporting, persistent losses, poorly documented intercompany transactions these are well-known audit triggers that regulatory authorities routinely target, particularly in transfer pricing examinations. The pattern is clear: many external risks that trigger audits actually originate from internal gaps you left unaddressed.

The Corporate Tax Risk Management Framework

Effective corporate tax risk management follows a structured framework that organizations can adapt to their specific circumstances and complexity levels.

This framework isn’t theoretical; it reflects how organizations successfully managing tax risk actually operate. The steps are sequential and iterative, creating a continuous cycle of assessment, action, and refinement.

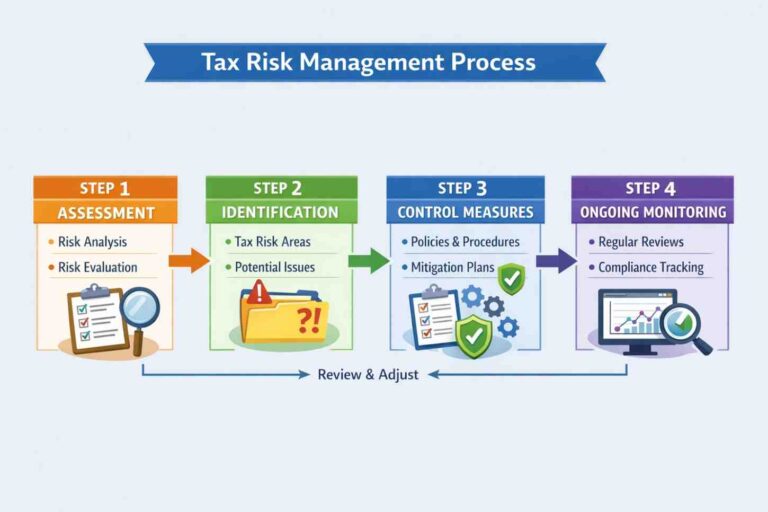

What Is the Tax Risk Management Process?

Most organizations managing tax risk well follow a four-stage approach that keeps repeating and improving over time.

First, assess where you stand. Review your compliance position, past filings, exposures, and whether your governance actually works as intended.

Second, identify and prioritize risks. Not every risk deserves equal attention. Catalog potential issues, then rank them by materiality, likelihood, and real impact.

Third, implement controls and mitigation. Put in place internal controls, documentation standards, and review procedures proportional to each risk level.

Fourth, monitor and review continuously. Track compliance performance, audit results, and regulatory changes. Adjust as needed.

This four-stage cycle forms the backbone of effective corporate tax risk management.

Step 1: Tax Risk Assessment of Current Tax Position

Managing tax risk starts with understanding where you are today. Your team can’t address risks they haven’t identified, which makes comprehensive assessment the foundation of everything following.

The assessment phase involves reviewing:

Filing Compliance Status

Filing compliance status across all jurisdictions where you have obligations. This means confirming all required returns have been filed, all amounts due have been paid, and you’ve identified and scheduled any outstanding obligations for resolution.

This sounds basic, but multi-jurisdiction operations often struggle with this step. Different entities, different filing requirements, different deadlines, different systems: things easily slip through the cracks. Starting with a complete inventory of what’s been filed and what’s outstanding creates clarity about baseline compliance status.

Tax Positions on Filed Returns

Positions you took on filed returns to evaluate whether they’re still defensible given current law, guidance, and enforcement trends. Tax positions that seemed reasonable when you filed returns might look different after regulatory guidance evolves or after audits test positions of other organizations.

This review should examine both routine positions you repeat year after year (often without much thought after the first time) and significant or unusual positions carrying material exposure if challenged.

Reserves and Financial Statement Disclosures

Reserves and disclosures in financial statements to ensure they appropriately reflect known uncertainties and probable liabilities. Accounting standards require you to evaluate uncertain tax positions and maintain reserves for amounts more likely than not to need adjustment. You need to update these assessments regularly as facts change.

Pending Disputes and Regulatory Matters

Pending or potential disputes with regulatory authorities, including understanding the status of any open audits, appeals, or litigation that could affect your tax position.

Business Operations Changes

Changes in business operations creating new tax obligations or affecting existing positions. Expansions into new jurisdictions, new product lines, new transaction types, structural changes, or significant commercial relationships all have potential tax implications requiring assessment.

Regulatory Environment Changes

Regulatory environment changes including new laws, regulations, court decisions, or administrative guidance affecting how you should evaluate your tax positions.

Assessment Outcomes

The assessment should result in documented understanding of:

- Where you stand on compliance obligations

- What significant tax positions you’ve taken and whether you’ve adequately supported them

- What known or potential exposures exist and how you’re managing them

- What changes in operations or regulations create new risks requiring attention

- Whether current reserves and disclosures appropriately reflect the risk profile

Such assessment creates the baseline for everything following. Without it, tax risk management efforts lack focus and direction.

Step 2: Risk Identification and Prioritization

Simple Tax Risk Assessment Template

Risk Area | Description | Impact | Control | Owner |

Once you understand your current position, the next step is systematic identification of risks and prioritization based on materiality and likelihood.

Not all tax risks are equal.

Some represent potentially significant financial exposure with reasonable probability of materialization. Others are theoretical possibilities with minimal practical likelihood or impact. Effective tax risk management requires distinguishing between these and allocating attention accordingly.

Risk identification involves examining each aspect of tax compliance and positioning to identify what could go wrong:

- What positions might regulatory authorities challenge?

- What documentation gaps exist that could make defensible positions indefensible?

- What process failures could result in missed deadlines or inaccurate filings?

- What changes in operations haven’t received full analysis from a tax perspective?

- What interpretive questions exist where your conclusion isn’t definitively supported?

The goal is creating a comprehensive inventory of potential risks, not solving them all immediately. Thoroughness matters in this step; risks you don’t identify can’t be managed.

Risk prioritization evaluates each identified risk across several dimensions:

Materiality measures the potential financial impact if the risk materializes. This includes direct tax exposure, penalties and interest, and potential secondary consequences like effects on credit agreements or regulatory standing.

Likelihood assesses the probability the risk will actually result in adverse consequences. Such assessment requires judgment about how regulatory authorities are likely to view positions, how well-supported positions are, and how actively different types of issues receive pursuit in the current enforcement environment.

Detectability considers whether the risk would receive identification through normal regulatory review processes or whether it’s likely to remain undetected absent specific scrutiny. More detectable risks may warrant more urgent attention.

Time horizon affects prioritization because some risks relate to current open tax years while others affect closed years where statutes of limitations are running or have expired.

Based on this analysis, risks receive categorization into priority tiers:

High priority risks carry material exposure with reasonable likelihood of materialization. These warrant immediate attention and active mitigation measures.

Medium priority risks have either moderate exposure or lower likelihood but still require monitoring and appropriate controls.

Low priority risks are theoretical possibilities with minimal realistic likelihood or impact. Documentation captures these but they don’t necessarily warrant significant resources.

Document the prioritization and review it with appropriate leadership so there’s shared understanding of what risks exist and how they’re being evaluated. Such documentation creates accountability and ensures tax risk management efforts align with organizational priorities.

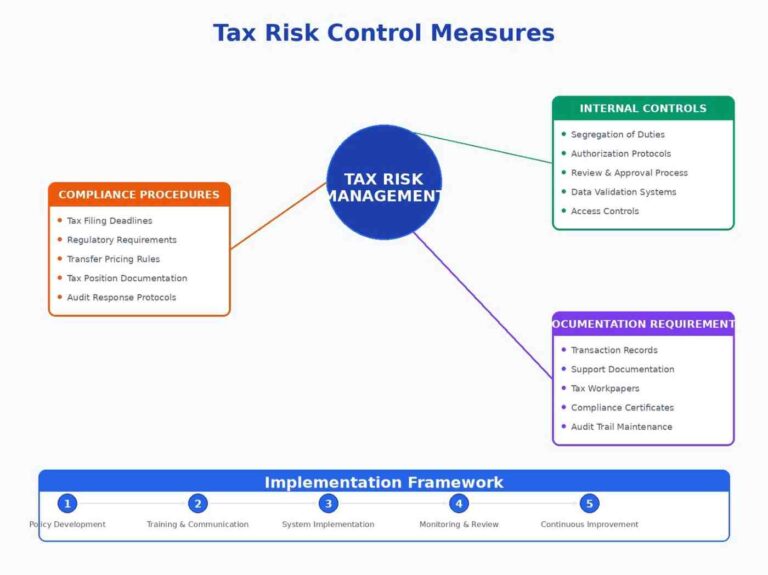

Step 3: Tax Risk Control and Mitigation Measures

Once you’ve identified and prioritized risks, the next step is implementing controls and mitigation measures proportional to the exposure.

Mitigation approaches vary based on risk type and priority:

For compliance and process risks, mitigation typically involves strengthening tax controls:

- Implementing compliance calendars tracking all filing obligations and triggering actions well in advance of deadlines

- Creating checklists and review procedures ensuring consistent handling of recurring compliance tasks

- Building data validation routines catching errors before information flows into tax calculations

- Establishing review and approval hierarchies preventing single-person errors from making it into filed returns

- Developing documentation standards specifying what support teams must gather for different types of positions

For interpretation and position risks, mitigation focuses on analysis and documentation:

- Conducting thorough technical research ensuring positions are well-grounded

- Documenting the reasoning and support for significant or non-routine positions

- Obtaining external opinions when positions involve material uncertainty or when independent validation adds value

- Implementing review processes where positions receive examination by multiple qualified professionals before your team files returns

- Establishing thresholds where positions above certain dollar amounts require additional scrutiny or approval

For transactional and structural risks, mitigation involves planning and coordination:

- Bringing tax into transaction planning early enough to influence structure rather than just documenting after the fact

- Conducting pre-transaction modeling to understand tax implications of different approaches

- Creating documentation contemporaneously rather than reconstructing later

- Implementing approval processes for significant transactions including tax sign-off as a required step

- Developing protocols for complex arrangements specifying documentation requirements and compliance obligations

For operational and resource risks, mitigation addresses capacity and systems:

- Investing in technology automating routine processes and reducing manual error risk

- Training personnel on tax risk awareness so issues receive appropriate escalation

- Creating documentation of key processes and positions so knowledge isn’t solely resident in individuals’ heads

- Establishing relationships with external resources providing surge capacity or specialized expertise when needed

- Building adequate time into schedules for proper review rather than forcing everything into last-minute compliance mode

The key principle is proportionality. High-priority risks warrant significant mitigation measures. Lower-priority risks may receive address through basic tax controls and monitoring without extensive resources.

Teams should document mitigation measures so there’s a clear record of what controls exist, how they operate, and who’s responsible for each aspect of tax risk management.

Step 4: Monitoring and Ongoing Review of Tax Risk

Tax risk management isn’t a one-time project; it’s an ongoing process requiring continuous monitoring and regular review.

Continuous monitoring involves tracking metrics indicating whether controls operate effectively:

- Compliance metrics showing whether your team makes filings timely and accurately

- Error rates in tax calculations or returns that might indicate quality control issues

- Audit results showing whether positions are holding up under review

- Process metrics showing whether steps in compliance workflows receive completion as designed

- Documentation metrics showing whether required support receives gathering and retention

When monitoring indicates problems, they should trigger investigation and corrective action rather than just receiving notation and being ignored.

Regular reviews create structured opportunities to step back from day-to-day execution and evaluate whether the overall approach is working:

Quarterly reviews can focus on compliance status, significant transactions or positions taken during the period, and any regulatory developments affecting tax risk assessment.

Annual reviews should be more comprehensive, covering the full risk assessment cycle, evaluating whether controls are appropriate given the current risk profile, and updating risk prioritization based on changes in operations or regulatory environment.

Post-audit reviews after any regulatory examination should analyze what worked, what didn’t, and what adjustments are needed to control, processes, or positions.

Document monitoring and review findings and report them to appropriate leadership. When you identify issues, there should be clear accountability for determining what actions are needed and ensuring they receive implementation.

The framework is cyclical; monitoring and review feed back into updated assessments, which inform revised risk prioritization, which drives adjustments to controls and mitigation measures. This continuous improvement cycle keeps corporate tax risk management aligned with organizational realities rather than becoming stale and disconnected from actual operations.

Many multinational organizations also align their internal tax governance practices with internationally recognized guidance. For example, the OECD’s cooperative compliance initiatives and tax risk management guidance, including programs such as the International Compliance Assurance Programme (ICAP), encourage structured engagement between companies and tax authorities to improve transparency and reduce uncertainty in tax administration.

Want to ensure your organization is audit-ready? Our team of tax risk specialists can help assess your current framework and identify opportunities to strengthen your tax risk management approach.

The Role of Tax Governance in Risk Management

Tax risk management operates within the broader context of corporate governance, and leadership oversight plays a critical role in whether tax risk receives effective management.

Organizations treating tax as solely a technical or compliance function, disconnected from governance and strategic oversight, often discover gaps when problems surface. Effective tax risk management requires clear tax governance structures establishing accountability, ensuring appropriate oversight, and integrating tax into broader corporate risk management.

What Tax Governance Means in Practice

Tax governance refers to the systems, processes, and oversight structures ensuring your organization’s tax obligations receive identification, understanding, and management in alignment with overall corporate principles and risk tolerance.

In practical terms, tax governance establishes:

Who is responsible for different aspects of tax risk management, from day-to-day compliance through strategic tax positions and overall risk oversight.

What standards apply to how you make tax decisions, how teams document positions, and what level of risk is acceptable.

How you report tax matters to leadership, what information flows to whom, and how you escalate significant issues.

Where tax fits within overall enterprise risk management and how it connects to financial reporting, regulatory compliance, and strategic decision-making.

Tax governance isn’t about creating bureaucracy. It’s about ensuring clarity around responsibilities and standards, so tax risk receives consistent and deliberate management rather than ad hoc handling based on whoever happens to be involved at any given moment.

Effective tax governance creates predictability. People know what’s expected, what authority they have, what requires escalation, and how decisions should receive documentation. Such clarity reduces risk coming from inconsistency or gaps in accountability.

Types of Risk Relevant to Corporate Tax

Corporate tax risk doesn’t exist in a vacuum. It touches multiple areas of enterprise risk, and understanding these connections helps you design controls that actually work rather than just checking boxes.

When you’re building or evaluating your tax governance framework, you’re really managing five interconnected risk types:

Compliance Risk

This is what most people think of first when they hear “tax risk.” It’s what happens when your organization fails to meet statutory obligations.

In practice, compliance risk shows up as late or inaccurate filings, incorrect calculations, missed reporting requirements, or inadequate documentation when auditors come knocking. It’s the most visible form of tax risk and typically results in penalties, interest charges, and unwanted regulatory attention.

Operational Risk

Operational risk emerges from weaknesses in your internal processes, systems, or people.

Think manual errors in tax calculations. Poor integration between your finance and tax systems. Inadequate review controls that let mistakes slip through. Staff turnover that takes critical knowledge out the door without proper documentation or transition.

Here’s the thing about operational weaknesses: they often create compliance failures indirectly. The root cause isn’t that you don’t understand the tax law; it’s that your processes can’t consistently execute what you know you need to do.

Financial Risk

Financial risk relates to the monetary impact of tax exposure on your organization.

This includes unexpected tax liabilities that hit your balance sheet, under-provisioning in financial statements that forces restatements, cash flow disruptions from assessments, and the accumulation of interest and penalties. Poor tax governance can materially affect earnings, credit ratings, and investor confidence.

Strategic Risk

Strategic risk arises when tax considerations don’t align with broader business decisions.

You see this when companies enter new markets without evaluating tax implications, structure transactions inefficiently, fail to anticipate regulatory reform, or take aggressive tax positions that conflict with long-term objectives. Tax should support your strategy, not undermine it.

Strategic tax risk often gets overlooked until a major transaction or restructuring reveals gaps between what the business wants to accomplish and what tax reality allows.

Reputational Risk

Reputational risk occurs when tax practices damage stakeholder trust.

In today’s environment, corporate tax behavior receives intense scrutiny from regulators, media, investors, and the public. Risk can arise from public disputes with tax authorities, perceived aggressive tax avoidance (even if technically legal), or governance failures revealed during audits.

Your reputation can take a hit even when your actions are technically compliant but appear poorly governed or inconsistent with stated corporate values.

Understanding these five risk types allows you to design targeted controls within your tax governance framework rather than applying broad, ineffective safeguards that create bureaucracy without actually reducing exposure.

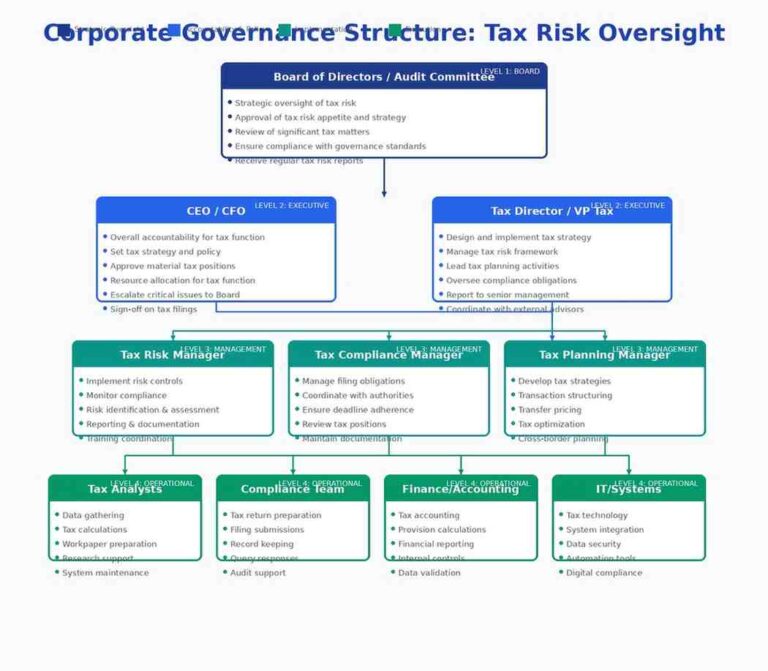

Board and Senior Management Oversight

While operational tax management happens at the staff and mid-management level, ultimate accountability for tax risk sits with senior leadership and the board.

Board oversight typically operates through the audit committee, which has responsibility for financial reporting integrity and risk management. The audit committee should receive regular reporting on:

- Your organization’s tax risk profile and significant exposures

- Material tax positions being taken and the basis for them

- Results of tax audits or regulatory examinations

- Adequacy of tax risk management processes and controls

- Any significant changes in tax strategy or risk tolerance

Board oversight isn’t about reviewing individual tax positions or making technical tax decisions. It’s about ensuring appropriate systems exist, that management is attending to tax risk, that significant exposures receive understanding, and that your approach aligns with overall governance principles.

Senior management responsibility for tax risk typically sits with the CFO, though some organizations assign specific tax risk oversight to other executives. Senior management is responsible for:

- Ensuring adequate resources and expertise are available for tax risk management

- Establishing policies and risk tolerance guiding tax decision-making

- Reviewing and approving significant tax positions or transactions with material tax implications

- Monitoring whether tax risk management processes operate effectively

- Ensuring tax matters receive appropriate reporting to the board

Leadership should document this oversight through regular reporting, review sessions, and sign-offs on significant decisions. Such documentation creates accountability and provides evidence that governance processes operate as intended.

Accountability and Reporting Structures

Clear accountability structures prevent tax risk from falling into gaps where everyone assumes someone else is handling it.

Operational accountability for day-to-day tax compliance and risk management typically sits with the tax director or head of tax, who is responsible for:

- Ensuring filings receive completion accurately and timely

- Identifying tax risks in operations and transactions

- Implementing and maintaining tax controls

- Coordinating with external advisors

- Reporting tax matters to senior management

Cross-functional accountability recognizes that tax risk management requires involvement from legal, finance, treasury, operations, and business units. Clear protocols should specify:

- When and how teams should consult tax on transactions or operational changes

- What information business units need providing to tax for compliance purposes

- How tax implications factor into business decision-making

- What escalation paths exist when you identify tax issues

Reporting structures should ensure tax matters flow to appropriate levels of leadership based on significance. Routine compliance updates might go to the CFO monthly or quarterly. Significant positions or exposures should receive escalation to the CEO or audit committee. Material tax disputes or investigations warrant immediate board notification.

The reporting should provide both detail (what specific issues exist and what’s being done about them) and summary (overall status, trends, key metrics) so different levels of leadership receive information appropriate to their oversight roles.

Alignment with Corporate Governance Principles

Tax governance shouldn’t exist in isolation; it should align with and reinforce overall corporate governance principles.

If your organization values transparency, tax governance should emphasize clear documentation, thorough reporting, and willingness to explain positions.

If your organization prioritizes integrity, tax governance should establish standards around how aggressively you take positions and what level of technical support teams must obtain before you adopt positions.

If your organization emphasizes risk management, tax governance should include robust tax risk assessment processes, appropriate controls, and conservative approaches to uncertain positions.

If your organization focuses on stakeholder value, tax governance should consider reputational implications and stakeholder expectations alongside technical tax analysis.

Alignment between tax governance and corporate governance principles helps ensure tax decisions reflect organizational values rather than existing in a separate silo where different standards apply.

It also ensures that when tax issues arise, they receive treatment not as disconnected compliance problems but as governance matters warranting appropriate attention and accountability.

Corporate Tax Risk and Audit Readiness

Tax audits are a normal part of corporate operations, but how well you handle them depends largely on how effectively you’ve managed tax risk before audits begin.

Tax audit readiness isn’t something you should think about when regulatory authorities show up. It’s a natural by-product of sound tax risk management practices that should already be in place.

How Unmanaged Tax Risk Leads to Audits

Regulatory authorities have limited resources and use risk-based selection to determine which organizations to audit. Several factors increase the likelihood your organization will receive selection for examination, and most relate directly to how well you’ve managed tax risk.

Inconsistencies in filings: across multiple years or across related entities raise questions. When returns show unusual year-to-year variations without clear explanations, or when affiliated entities report positions not seeming to align, regulatory authorities want understanding what’s driving the inconsistencies.

Positions deviating from norms: for the industry or size of organization draw attention. While legitimate differences exist, positions appearing outlier relative to peers often trigger examinations to verify they’re appropriate.

Late filings, amendments, or corrections: suggest process problems regulatory authorities want understanding better. Organizations consistently missing deadlines or needing to amend returns are showing signs of weak controls that might extend to substantive tax positions.

Participation in transactions or structures: that are known areas of focus for regulatory enforcement can increase examination likelihood. This doesn’t mean the transactions are problematic, but it means they’re receiving scrutiny.

Prior audit adjustments: increase the likelihood of subsequent examinations, especially if adjustments were material or covered similar issues across multiple years.

Industry-specific risks: in sectors that are enforcement priorities or that have unique compliance challenges often face higher audit rates regardless of organization-specific factors.

Your team can’t eliminate audit risk entirely, but organizations with strong tax risk management practices tend to face fewer audits and better outcomes when examined because they don’t exhibit the signs triggering regulatory concern.

Documentation and Defensibility

When audits do occur, outcomes depend heavily on the quality of documentation supporting positions you took on returns.

Regulatory authorities expect contemporaneous documentation: records created when transactions occurred and positions were determined, not materials reconstructed after audit questions arise.

Transaction documentation should capture:

- What the transaction accomplished from a business perspective

- Why it received structuring the particular way it did

- How pricing or terms were determined

- What alternatives received consideration

Position documentation should explain:

- What tax rules or authorities support the treatment

- How the facts of the specific situation map to those rules

- What interpretive questions existed and how they received resolution

- Whether you considered alternative positions and why you rejected them

Process documentation demonstrates positions weren’t taken casually but resulted from deliberate analysis and appropriate review.

The quality of documentation often determines whether positions survive scrutiny. Even technically correct positions may not hold up if they can’t receive adequate explanation and support. Conversely, positions that might receive questioning from a pure technical perspective often survive when thorough documentation demonstrates they were taken based on reasonable interpretation of ambiguous rules.

Documentation doesn’t guarantee positions will receive sustainment, but lack of documentation almost guarantees positions will face challenge and often adjustment.

Strong documentation practices are essential for audit readiness. Tax authorities expect organizations to maintain clear records supporting their tax positions, calculations, and compliance processes. Guidance from regulatory authorities such as the IRS recordkeeping requirements emphasizes the importance of maintaining organized documentation to substantiate tax filings and defend positions during regulatory reviews.

Audit Readiness as a By-Product of Good Risk Management

Organizations having implemented sound corporate tax risk management frameworks typically find themselves audit-ready without special preparation.

When tax risk management includes:

- Regular assessments of positions for defensibility

- Documentation standards requiring contemporaneous support

- Review processes examining positions before filing

- Controls ensuring accuracy and completeness of filings

Then audit readiness exists as a natural state rather than something requiring scrambling when examinations begin.

Tax audit readiness means:

Your team can quickly locate documentation supporting positions you took on returns without extensive searching or reconstruction.

Positions appearing questionable received intentional adoption based on documented analysis, not accidental acceptance without consideration.

Process controls provide evidence filings received proper review and approval, reducing concerns about careless errors.

Relationships between your filings and underlying financial records can receive easy reconciliation and explanation.

Personnel who handled original transactions or positions are still available (or their work receives sufficient documentation that others can explain it).

Organizations maintaining tax audit readiness as an ongoing state handle examinations far more efficiently and with better outcomes than organizations needing to reconstruct support reactively after questions arise.

Regulatory Expectations During Reviews

Understanding what regulatory authorities expect during audits helps you prepare appropriately and respond effectively.

Information requests: should receive complete and prompt answers. Delayed responses or incomplete information increase scrutiny and extend examination timelines.

Explanations: should be clear, accurate, and consistent. When different people provide inconsistent explanations for the same position, it raises concerns about whether the position received careful consideration.

Cooperation: doesn’t mean accepting all proposed adjustments, but it does mean engaging professionally, providing requested information, and explaining positions candidly rather than stonewalling.

Technical support: for positions should be substantive, not just formulaic citations. Regulatory authorities expect you to be able to explain why specific authorities apply to specific facts, not just list general references.

Professionalism: in audit interactions matters. Organizations treating examiners respectfully and providing organized, thorough responses tend to have more constructive examination experiences than organizations that are defensive, dismissive, or disorganized.

Regulatory expectations have increased as authorities have become more sophisticated. Simple assertions that positions are correct aren’t sufficient; you need demonstrating through documentation, explanation, and transparency that positions were taken thoughtfully and are grounded in reasonable interpretation of applicable rules.

Organizations with strong tax risk management practices meet these expectations naturally because their normal processes already produce the analysis, documentation, and support regulatory authorities expect seeing.

Building a Sustainable Tax Risk Management System

Effective tax risk management doesn’t happen through one-time projects or periodic fixes. It requires systematic approaches becoming embedded in how you operate.

Building sustainability into tax risk management ensures practices persist through personnel changes, organizational growth, and evolving complexity rather than degrading over time until problems force reactive attention.

Systems vs One-Time Compliance

Many organizations approach tax risk management episodically: addressing issues when they’re identified, fixing problems after audits, or conducting periodic reviews without systematic follow-through.

Such an approach creates cycles of attention and neglect. Risk management improves temporarily when problems surface or during focused initiatives, then gradually degrades as attention shifts to other priorities and discipline wanes.

Sustainable systems operate differently through:

Standard processes: defining how you identify, analyze, document, and fulfill tax obligations consistently regardless of who’s involved or what else is competing for attention.

Technology platforms: automating routine tasks, enforcing workflow steps, maintaining compliance calendars, and preserving documentation systematically rather than relying on individual discipline.

Defined roles and responsibilities: ensuring specific people are accountable for specific aspects of tax risk management, with clear escalation paths and backup coverage preventing gaps when personnel change.

Regular cadences: for assessments, reviews, and reporting ensuring tax risk receives ongoing attention rather than only when crises arise.

Quality metrics: tracking whether processes operate as designed and whether outcomes meet standards, creating visibility into performance trends.

Systems create consistency and sustainability. They reduce dependency on specific individuals or heroic efforts and make sound tax risk management the path of least resistance rather than something requiring constant vigilance to maintain.

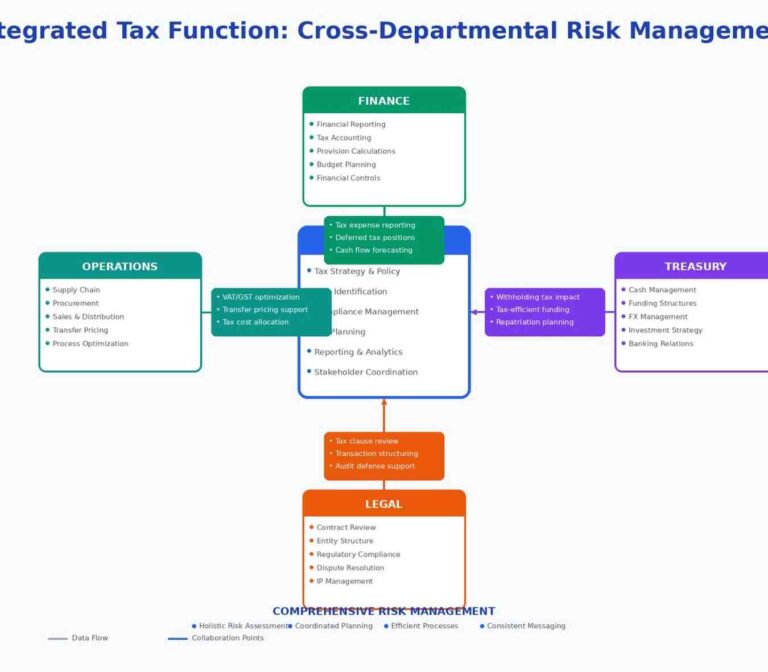

Integration with Finance and Operations

Tax risk management can’t operate effectively in isolation from broader finance and business operations.

Integration with financial reporting ensures tax matters receive consideration as part of close processes, that tax reserves and disclosures stay current, and that tax implications receive understanding when you analyze or present financial results.

Many organizations discover tax issues when financial statements are being finalized because tax wasn’t adequately involved in earlier stages of financial reporting. Building tax into regular close processes prevents last-minute surprises and ensures tax considerations inform financial reporting throughout the cycle.

Integration with treasury is critical because financing decisions, cash management, intercompany transactions, and foreign exchange activities all carry tax implications needing to receive understanding and proactive management.

When tax and treasury don’t coordinate effectively, you make decisions creating unnecessary tax complications or miss opportunities to structure activities more efficiently from a tax perspective.

Integration with legal matters because many transactions, contracts, and structural decisions have both tax and legal dimensions needing consideration together.

Decisions making sense from a legal perspective might create tax complications and vice versa. Joint consideration of tax and legal implications leads to better overall outcomes than sequential analysis where each discipline examines issues independently.

Integration with business operations

This means bringing tax into planning discussions early enough to influence decisions rather than just documenting after the fact.

The most common complaint from tax professionals is they learn about transactions too late to provide meaningful input. By the time tax becomes involved, commercial deals receive finalization, structures are set, and tax’s role is limited to compliance rather than planning.

Organizations integrating tax into front-end business processes through defined consultation requirements, transaction approval workflows, or representation in planning discussions create better outcomes and reduce surprise issues.

Integration doesn’t mean tax has veto power over business decisions. It means tax considerations receive understanding and appropriate weighing in decision-making rather than being ignored until compliance requirements force attention.

Role of Technology and Process Discipline

Technology enhances tax risk management by automating routine tasks, enforcing process discipline, and providing visibility that would be difficult maintaining manually.

Tax compliance software can automate calculation of tax liabilities, preparation of returns, tracking of filing requirements across jurisdictions, and maintenance of compliance calendars triggering actions at appropriate times.

Such automation reduces manual effort, minimizes calculation errors, and ensures routine compliance obligations don’t receive missing due to oversight.

Document management

These systems provide structured repositories for tax-related documentation with retention policies, search capabilities, and access controls ensuring documentation receives preservation appropriately and can be located efficiently when needed.

Many documentation problems stem from poor organization rather than lack of documentation. Systematic document management addresses this by making documentation preservation and retrieval routine rather than dependent on individual filing practices.

Workflow tools enforce process steps by requiring specific actions, approvals, or documentation before activities can proceed to next stages.

This process discipline prevents shortcuts or gaps occurring when individuals bypass steps due to time pressure or competing priorities.

Data analytics and reporting tools provide visibility into tax metrics, compliance status, and risk indicators through dashboards and regular reports highlighting areas requiring attention.

Such visibility helps management understand whether tax risk receives effective management and spots emerging issues before they become significant problems.

Technology alone doesn’t create effective tax risk management; it requires appropriate processes, trained personnel, and organizational commitment. But technology amplifies the effectiveness of good processes and makes sustainable execution more achievable.

Process discipline matters as much as technology. Clear standards for how work receive performance, documentation, and review create consistency persisting across personnel changes and volume fluctuations.

Documentation of standard processes through written procedures, training materials, and checklists ensures institutional knowledge isn’t solely in people’s heads and that quality doesn’t depend entirely on individual expertise.

Continuous Improvement Mindset

Even well-designed tax risk management systems need ongoing refinement as operations change, regulations evolve, and learning occurs through experience.

Post-audit learning should capture lessons from examinations and incorporate them into processes and controls. When audits identify issues, the question shouldn’t just be how to resolve the specific matter, but what process improvements would prevent similar issues in the future.

Regulatory change management requires monitoring developments in tax law and enforcement and assessing implications for existing positions and processes. As regulations change, tax risk management approaches need evolving to address new requirements and risks.

Process review and refinement based on metrics, user feedback, and operational experience helps identify where processes aren’t working as intended and where adjustments would improve effectiveness or efficiency.

Benchmarking and comparison against peer practices or industry standards provides perspective on whether your approaches are appropriate or whether different methods might work better.

Organizations treating tax risk management as static eventually find their systems becoming outdated and less effective. Organizations embracing continuous improvement maintain relevance and effectiveness even as complexity increases and environments change.

Continuous improvement doesn’t mean constant major overhauls. It means regular incremental refinements keeping systems aligned with current needs and incorporating learning from experience.

International organizations are developing comprehensive frameworks for tax cooperation and risk management. The United Nations Framework Convention on International Tax Cooperation provides guidance on coordinated approaches to tax governance and cross-border compliance challenges, offering valuable perspective for organizations operating in multiple jurisdictions.

Key Takeaways for Organizations

Corporate tax risk management doesn’t require perfection, but it does require intentionality and structure.

Tax risk exists in every organization regardless of size, industry, or complexity. The question isn’t whether you have tax risk; it’s whether you’re managing it deliberately or hoping nothing goes wrong.

Proactive frameworks reduce exposure by identifying risks before they materialize, implementing controls proportional to exposure, and creating visibility allowing informed decision-making.

Organizations waiting until problems surface find themselves managing in crisis mode with fewer options and higher costs than organizations addressing risks proactively.

Governance and systems matter more than technical perfection. No organization can eliminate all tax risk or achieve every position perfectly right. What distinguishes effective tax risk management is having systems identifying issues, controls preventing common failures, documentation supporting positions, and governance ensuring appropriate oversight.

Confidence comes from structure, not guesswork.

Organizations with sound corporate tax risk management frameworks can make business decisions confidently because they understand their tax positions, know their documentation is solid, and have processes catching issues before they become problems.

Such confidence enables better strategic decision-making, more efficient audit processes, and stakeholder trust that you’re managing obligations responsibly.

Tax risk management isn’t about complexity or sophistication; it’s about discipline, documentation, and deliberate attention to an area affecting financial performance, regulatory standing, and organizational reputation.

Organization treating task risk as a governance priority rather than just a compliance function creates sustainable value through reduced exposure, better decision-making, and confidence that obligations receive appropriate management.

Frequently Asked Questions About Corporate Tax Risk Management

What is corporate tax risk management?

Corporate tax risk management is the systematic process organizations use to identify, assess, and mitigate risks related to their tax obligations and positions, including compliance risks, interpretation uncertainties, and potential financial exposures.

Why is tax risk management important for organizations?

Tax risk management protects organizations from financial penalties, regulatory scrutiny, and reputational damage while ensuring compliance obligations are consistently fulfilled. It also supports better business decision-making by providing clarity about tax positions and potential exposures.

How do organizations identify tax risks?

Organizations identify tax risks through regular tax risk assessments, internal control reviews, monitoring regulatory changes, analyzing new transactions, and maintaining open communication between tax teams and business units.

What are common sources of corporate tax risk?

Common sources include compliance and filing errors, interpretation of complex tax laws, inadequate documentation, transactional and structural complexities, and operational process failures.

How often should organizations conduct tax risk assessments?

Organizations should conduct comprehensive tax risk assessments at least annually, with quarterly reviews of compliance status and significant transactions. High-complexity organizations or those experiencing rapid change should assess more frequently.

What role does documentation play in tax risk management?

Documentation is critical for defending tax positions during audits. Contemporaneous documentation created when transactions occur provides support needed to demonstrate that positions were taken thoughtfully and based on reasonable interpretations.

Organizations managing complex tax and regulatory obligations often benefit from structured advisory support when designing or reviewing tax risk management frameworks. Professional tax advisors can provide specialized expertise, independent perspectives, and experience across different industries and regulatory environments complementing internal capabilities.

Contact our advisors today to strengthen your corporate tax risk management framework and gain confidence in your tax positions.

If you’re evaluating your organization’s approach to corporate tax risk management or want to strengthen existing frameworks, consider reaching out to advisors who can assess your current state and help develop approaches tailored to your specific circumstances and risk profile.